Smart SIP: Spend-Calibrated Investment Recommendations on CRED Invest

Outcome

≥35% SIP initiation among recommendation-exposed users at M1; ≥70% still active at M3

Strategic Fit

The company bet

CRED acquired Kuvera in February 2024 for a specific reason: it had 13 million users, most of them credit card holders with credit scores above 750, and none of them investing through CRED.1 The Kuvera acquisition gave CRED a SEBI-registered RIA, a direct MF platform, and a team of 50 with wealth management expertise.2

The bet is simple. CRED's user base is exactly the demographic that should be running SIPs: urban professionals, high credit scores, clearly able to commit to a monthly outflow. The product doesn't convert them. CRED Invest exists. The activation problem doesn't.

Why now

Three signals from the last year make this the right moment.

Signal 1: SIP churn is getting worse, not better. The SIP stoppage ratio, the count of discontinued SIPs against new registrations, sat at 74.83% in January 2026, rose to 75.62% in February, and hit 76% in March, with nearly 50 lakh SIPs paused or terminated against 65.7 lakh new ones.3 It has stayed above 70% for most of the last two years.4 People keep starting SIPs and abandoning them, and no platform has structurally fixed it.

Signal 2: the cause is a miscalibrated amount, not disengagement. The most common way a SIP dies is an insufficient balance on the NACH debit date.5 Under SEBI rules effective April 2024, two consecutive failed debits cancel the SIP automatically.6 Someone who set a ₹10,000 SIP in a month where they actually had ₹6,000 of surplus didn't lose interest in investing. They got bounced, paid their bank ₹250–₹750 for the failed debit, and started over.7 The amount was wrong on day one.

Signal 3: CRED has the one input that fixes this, and it's sitting idle. Groww took 47% of all new SIP registrations in October 2025 with a clean UI and zero data on what its users actually spend.8 CRED has category-level monthly spend, credit-utilisation history, and payment behaviour, which is exactly what a financial planner would use to set a sustainable SIP amount. No pure-play MF platform can see this. CRED isn't using it.

Strategic risk if this doesn't ship

CRED Invest competes with Groww, Zerodha, and Kuvera's own direct MF offering. With no differentiated hook, it's a worse version of all three: less SIP volume than Groww, less depth than Zerodha, a thinner power-user base than Kuvera on its own. The spend-data angle is the only feature asymmetry CRED has here. If it never gets productised, the wealth-management thesis behind the Kuvera acquisition doesn't land.

User and Problem Statement

Primary user

Priya, 29, product manager at a Bengaluru SaaS company. Monthly salary credit of ₹1.1 lakh. Credit card spend of ₹55,000–₹70,000/month across dining, travel, and lifestyle. CIBIL score 780. Has a CRED account, uses it to pay her credit card bill on time for the reward points. Has thought about starting a SIP at least twice in the last year. Has not started one.

The friction isn't access or awareness. It's the amount question: how much should I invest? Every platform she's opened, Groww, Scripbox, her bank's MF section, asks for her income and her goal, runs a formula, and hands back a number that feels arbitrary. She has no way to know whether ₹8,000 a month is sustainable for her or reckless. So she puts it off again.

Secondary user

Rohan, 34, has run a SIP for 14 months. He started at ₹5,000 a month when he joined his current company, got promoted eight months ago, and his spending is up 20–25% since. The SIP hasn't moved, and no platform has flagged the gap. His investment is calibrated to a financial reality that's 14 months out of date.

The problem in users' voices

"Every app asks me my salary and my goal and gives me a number. But I don't know if that number makes sense for how I actually live. I always end up not starting because I'm not sure I can commit to it every month."

Here's the structural gap. Every MF platform sets a SIP amount from what you earn and what you want to achieve. None of them look at what you actually spent last month. The roughly 75% of new SIPs that stop within two years, a figure that holds across AMFI reporting, largely trace back to amounts that were never calibrated to real spending capacity.9

Today's workaround

Users either pick a round number like ₹5,000 or ₹10,000 with no reference to their cash flow, or they don't start at all. The not-starting is the bigger problem. CRED's gap is full of users who intend to invest and haven't, not users who tried and left.

Goals and Non-Goals

- Convert CRED users who have not started a SIP, using spend data as the activation hook

- Reduce SIP abandonment at M3 by setting an amount calibrated to actual discretionary capacity

- Reduce time from recommendation view to confirmed SIP to under 60 seconds

- Drive average Smart SIP ticket to ≥₹5,000/month (matching Kuvera's user average)

- Build the spend-data recommendation engine as an internal platform asset, reusable for future wealth products

- Full robo-advisor or portfolio management, out of scope for v1

- Real-time rebalancing, tax optimisation, or goal planning

- Stock, direct equity, or derivative recommendations

- Account Aggregator integration in v1; spend data comes from the CRED internal API only

- Recommending specific fund schemes by name where it would trip SEBI's investment-advisory boundary; categories only until legal clears

User Stories

As a First-time investor on CRED

I want to see a personalised SIP amount based on my actual spending, not an income formula

So that I don't have to research mutual funds or guess whether I can sustain the amount

Acceptance Criteria

As a Existing SIP investor on CRED (12+ months, amount unchanged)

I want to be prompted to review my SIP when my spending capacity has grown materially

So that my monthly investment reflects current income, not a 14-month-old decision

Acceptance Criteria

As a User whose SIP failed due to insufficient balance

I want to understand why it failed and restart with an amount I can actually maintain

So that I don't lose compounding time and don't pay bank bounce penalties again

Acceptance Criteria

Functional Requirements

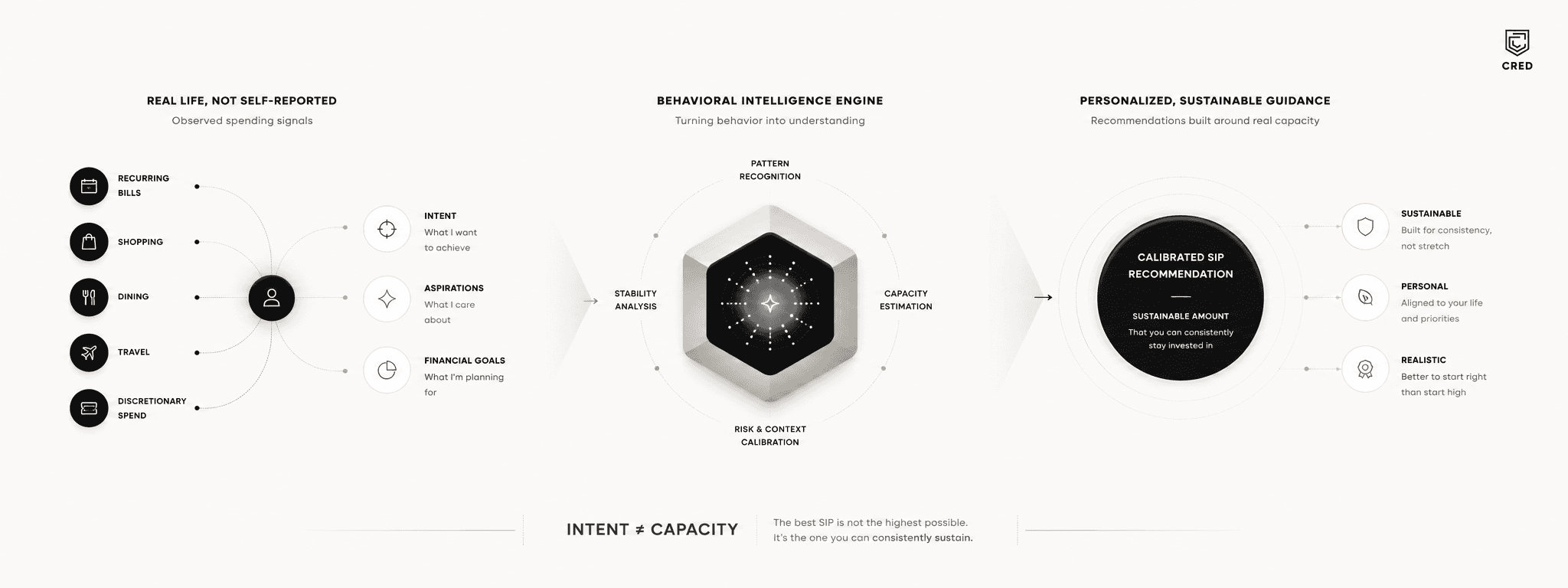

Recommendation engine

Smart SIP derives the suggested amount from three layers:

The base layer uses CRED's internal spend data: average monthly card spend by category (discretionary vs. essential), payment timing relative to month-end, and the credit-utilisation trend over the past six months. From that it computes an estimated monthly surplus as a proxy for investable capacity. The category split is configurable. The current assumption treats dining, travel, entertainment, and lifestyle as discretionary, and rent, utilities, insurance, and EMIs as essential.

The allocation layer applies a band of 20–30% of the computed surplus, lower bound for volatile cash flow and upper bound for stable. The band is configurable through a feature flag, with no app release needed.

The fund selection layer reads the user's inferred risk profile, drawn from credit-utilisation stability, spend volatility, and a single self-classification question on first use, and surfaces up to three fund-category suggestions such as large-cap equity, balanced hybrid, or short-duration debt.

NOTE

If fewer than 60 days of CRED spend data exist for a user, confidence falls below threshold and the engine falls back to a goal-based input form. Do not surface a low-confidence algorithmic recommendation. A bad recommendation that fails at M3 is worse for retention than no recommendation at all.

API dependencies

- BSE StAR MF. SIP registration, amount modification, e-NACH mandate authentication. Failure mode: graceful degradation with queued retry, no partial order state written.

- CAMS / KFintech RTAs. Existing folio data, KYC status checks. Failure mode: cached portfolio snapshot (max 24h stale) with a staleness indicator.

- NPCI NACH via Decentro. Mandate registration and debit. Industry mandate failure rate ~8%, an expected path rather than an exception.

- CRED Internal Spend Data API. Primary input for the recommendation engine. Failure mode: fall back to the goal-based input form.

- Does a clean category-level spend aggregation API exist in CRED's data platform callable in real time, or does the engine need a batch pipeline? Latency and freshness directly affect recommendation accuracy.

- When a step-up recommendation exceeds the registered NACH mandate limit, what is the technical path for mid-SIP mandate upgrades via BSE StAR MF?

Success Metrics

Primary metric: SIP initiation rate at M1 among users who saw a Smart SIP recommendation. Baseline is zero (feature doesn't exist). The 35% target is benchmarked against Kuvera's observed conversion rates for high-intent users on direct MF platforms, adjusted down for the lower-intent CRED user who hasn't actively sought out investing.

Guardrail metrics (must not regress):

CRED Invest overall DAU

Smart SIP should not cannibalise existing Invest engagement

NACH mandate failure rate on execution

Above 15% = feature pause, root cause analysis

Recommendation edit rate

High edit rate = recommendation confidence failure

SIP-related support tickets

Risks, Open Questions, and Dependencies

| Type | Description | Owner | Deadline |

|---|---|---|---|

| Risk, Regulatory | Does algorithmically personalised SIP amount recommendation cross into SEBI-regulated investment advisory territory requiring RIA registration? Kuvera holds RIA status; CRED applied for IA licence separately. This boundary determines whether v1 can use the word "recommend" and surface fund categories at all. | Legal / Compliance | Sprint 1 |

| Open Question, Data | What is the minimum transaction history for a reliable recommendation within ±15% of a financial planner's manual estimate? The 60-day threshold is an assumption, not a validated floor. Data Science needs to run a backtesting exercise on Kuvera's existing user base. | Data Science | Sprint 2 |

| Open Question, Engineering | Does a real-time category-level spend API exist in CRED's data platform, or does the recommendation engine require a batch pipeline with hours of lag? This decision determines whether recommendations are session-fresh or daily-fresh. | Data Platform Engineering | Sprint 2 |

| Risk, UX | Step-up nudges for existing investors that breach the registered NACH mandate limit require a re-mandate flow through BSE StAR MF. Expected drop-off at this step is unknown. If it's above 40%, the step-up feature becomes net negative for AUM. | Engineering + Product | Sprint 3 |

| Dependency, Legal | Can CRED surface fund category shortlists (not scheme names) without additional AMFI/SEBI disclosure? This boundary determines the v1 recommendation output format. | Legal / Business | Sprint 2 |

Out of Scope

Items explicitly not in v1, listed here to prevent mid-execution scope arguments:

- LLM-generated financial planning commentary or personalised investment rationale beyond a single sentence

- Account Aggregator integration. v1 uses CRED internal spend data only; AA adds bank-statement richness but also consent complexity, so it is deferred to v2

- Portfolio rebalancing or goal tracking. Separate product surface, different team

- Stock, ETF, or direct-equity recommendations. Requires different regulatory clearance

- Specific scheme names in the recommendation. Pending a legal determination on the advisory boundary; categories only at v1

- Mid-SIP top-up or lump-sum integration. Adjacent feature, different NACH flow, a v1.1 candidate

Footnotes

-

TechCrunch, "India's CRED to acquire mutual fund startup Kuvera," February 2024. https://techcrunch.com/2024/02/06/cred-acquires-mutual-fund-startup-kuvera-in-wealth-management-push/ ↩

-

Entrackr, "CRED acquires Kuvera to enter wealth management space," February 2024. https://entrackr.com/2024/02/cred-acquires-kuvera-to-enter-wealth-management-space/ ↩

-

AMFI monthly data via Finnovate and Republic World. SIP stoppage ratio of 74.83% (Jan 2026), 75.62% (Feb 2026), and ~76% (Mar 2026, ~50 lakh discontinued against 65.7 lakh new). https://www.finnovate.in/learn/blog/february-2026-sip-inflows-and-stoppage-ratio ↩

-

Finnovate, "Contributing SIPs Cross 94%: SIP stoppage ratios remain above 70%," July 2025. https://www.finnovate.in/learn/blog/sip-stoppage-contributing-sips-trend-2025 ↩

-

BusinessToday, "SIP payment failures can cost you up to Rs 2,950 per month," April 2026. https://www.businesstoday.in/mutual-funds/story/sip-failures-on-nach-mandate-can-cost-you-up-to-rs-2950-per-month-heres-how-524935-2026-04-09 ↩

-

Outlook Money, "If You Miss Two SIP ECS, Your SIP Will Get Cancelled," effective April 1, 2024. https://www.outlookmoney.com/invest/mutual-funds/if-you-miss-two-sip-ecs-your-sip-will-get-cancelled ↩

-

BusinessToday, April 2026 (ibid). Banks charge ₹250–₹750 per failed NACH debit. ↩

-

Indian Startup News, "Groww beats Zerodha, Angel One in new SIP registrations," December 2025. https://indianstartupnews.com/news/groww-beats-zerodha-angel-one-phonepe-in-new-sip-registrations-adds-over-2-million-new-sips-in-october-10879201 ↩

-

Tata Mutual Fund, "Decoding SIP Trends in Mid-2025." SIP stoppage ratios have remained elevated throughout 2024–2025. https://www.tatamutualfund.com/blogs/decoding-sip-trends-mid-2025-are-investors-consolidating-or-expanding-their-sips ↩