The Credit Invisible Problem: Why BNPL Underwriting Breaks for 300M Indians

Outcome

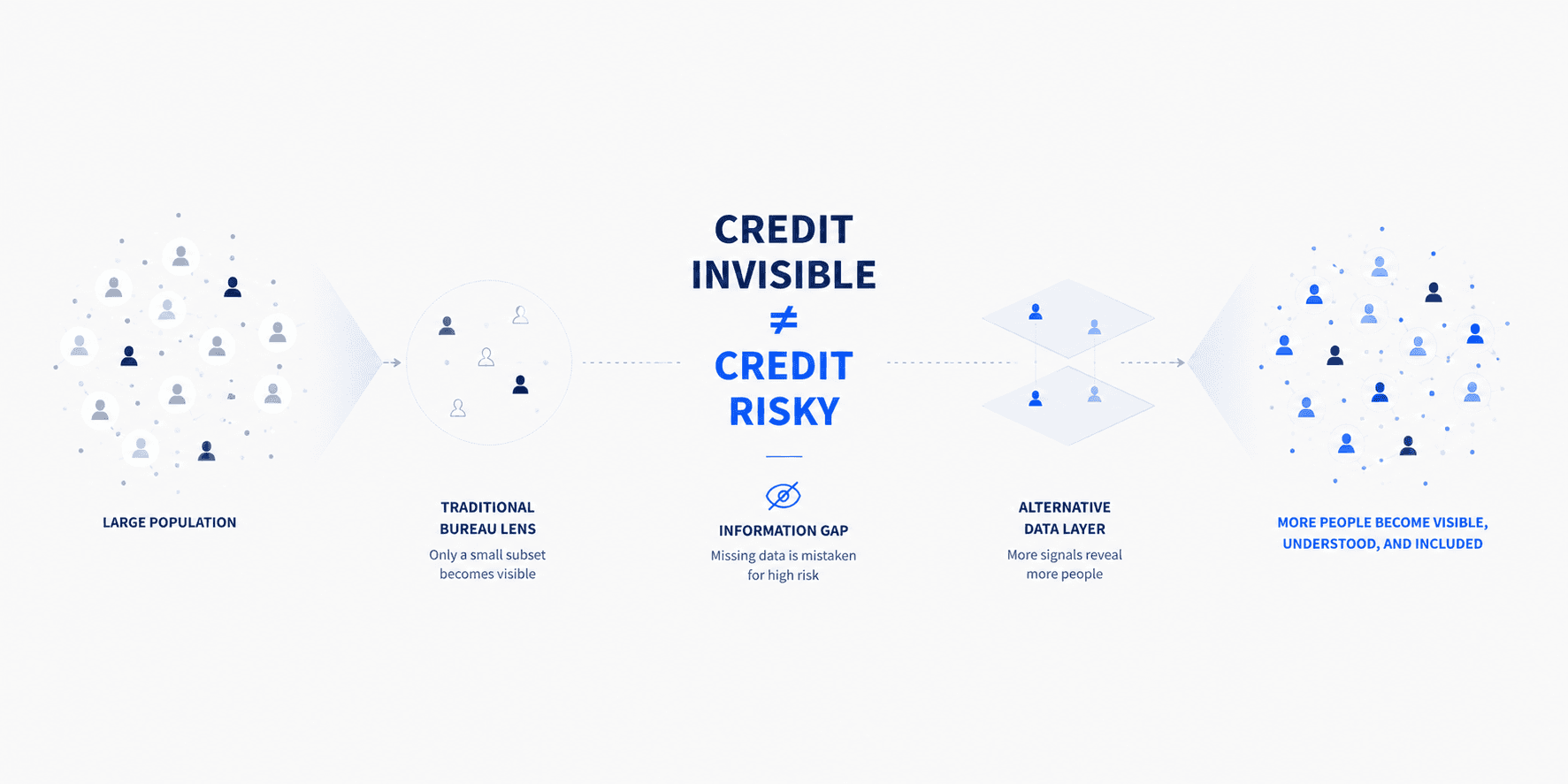

The thin-file problem is a product design choice, not a data limitation. An AA-native limit engine can remove bureau dependence for millions of eligible users.

What They Built

Around 300 million Indians can't get formal credit. Not because they're bad borrowers, but because no bureau has ever heard of them. A PayU executive put it bluntly in 2022: the top 30 million consumers get all the fun, and the remaining 300 million get almost no access.1 The pattern holds in the bureau data. TransUnion CIBIL's late-2024 reading has Gen Z at 34% of the credit-eligible population but the lowest credit penetration of any cohort, around 16%.2 Among rural and informal-sector workers it barely registers.

BNPL was meant to fix this. The bet was clean: use digital signals like UPI behaviour, device fingerprints, and KYC data to underwrite the people the bureau ignores. Skip the scorecard, approve at checkout, build a credit history from zero. Slice built its whole thesis on it, going after 20-year-olds and students who'd never held a card.

INSIGHT

The pitch was financial inclusion at internet speed. The reality is that most BNPL underwriting is still bureau-first, with alternative data bolted on as a fallback rather than the foundation. When the bureau comes back with "no score," the logic quietly fails over, and the user gets declined, throttled, or handed a ₹5,000 limit that won't cover a phone case.

What's Working

The real progress runs through India's Account Aggregator (AA) framework, which RBI launched in 2021. By the end of 2024 the network had roughly 120 million linked accounts, up from 39 million a year earlier, and had enabled over $10 billion in loans.3 Among people who'd applied for a loan, 21% recalled using AA data in 2024, double the 10% from 2023.4 One AA pull hands a lender 6–12 months of real bank-statement data: salary credits, EMI patterns, balance floors, all under explicit borrower consent and with no bureau in the loop.

UPI history is the other signal gaining ground. PayU has said its network gives it a depth of customer payment data that lets it pre-underwrite before a user even applies.5 FinBox runs AA feeds alongside thousands of device and transaction signals to score thin-file borrowers, and lenders like KreditBee, EarlySalary, and CASHe have built their own models on similar inputs for young or blue-collar applicants the bureau can't see.6

What's Broken

The deepest failure is bureau dependency. Most BNPL underwriting still leads with the bureau score and treats alternative data as a tiebreaker. When a first-time applicant comes back "no data" from CIBIL or CRIF, the fallback isn't a richer model. It's a lower limit or a hard decline.

NOTE

This isn't a data shortage. An AA pull on a 24-year-old with six months of steady salary credits tells you more about repayment than a bureau with nothing to return. The bureau stays first because the underwriting models were trained on bureau data, and retooling them carries credit-risk accountability nobody wants to sign their name to.

The limit-too-low failure gets less attention than it deserves. Slice ran ₹10,000 starting limits and held 90-day delinquency at 3.2%, a clean risk number bolted onto a broken product.7 A ₹10,000 limit won't cover a mid-range phone or a return domestic flight. Users who can't transact for anything meaningful don't build history, and users who don't build history never qualify for an upgrade. The product fails its own inclusion mission before anyone misses a payment.

ZestMoney, which wound down in 2023, asked for co-signers and extra documents even when bureau data existed. Neither its underwriting nor its collections model was built for the user it claimed to serve.

What I'd Ship

The highest-leverage fix is the limit-too-low problem, specifically the inability to raise limits for thin-file users who are visibly performing.

DECISION

An AA-native limit-escalation engine that takes the bureau out of post-approval limit decisions entirely. The initial limit is set from alternative data at onboarding, then escalation runs on 90-day AA refresh cycles with no bureau pull. Steady salary credits, no overdraft events, and on-time repayments trigger automatic increases in ₹5,000–₹10,000 steps, capped at ₹50,000 before a manual review.

Target user: thin-file borrowers aged 22–30, salaried or gig-employed, with at least three months of bank-account history reachable via AA consent.

Hypothesis: users who cross ₹20,000 in available limit within 90 days of approval transact at twice the rate of users stuck at ₹10,000, with no statistically significant rise in 30-day delinquency.

The PM Signal

India's credit infrastructure was built for the 30 million who already had access. BNPL's original bet, that digital signals could stand in for the bureau for the other 300 million, was right. Most products hedged it anyway. They kept the bureau at the top of the stack and used alternative data only to justify small limits on accounts they were still scared to own. The AA framework has taken that excuse off the table. What's left is a choice: build underwriting around your own signals, or keep treating them as a fallback. In a market where the data infrastructure has outrun the lenders' nerve, the real product decision is whether you trust your own signals enough to commit to them. Most BNPL players built the infrastructure and then kept reaching back for the bureau. That's the tell.

Footnotes

-

PayU India leadership, on the credit-access gap, 2022, widely cited in fintech coverage of India's underserved-borrower problem. ↩

-

TransUnion CIBIL, Credit Market Indicator, reported March 2025 (Q4 2024 data). Gen Z is ~34% of the credit-eligible population with the lowest credit penetration of any cohort, ~16%. https://newsroom.transunioncibil.com/41-of-first-time-borrowers-are-gen-z-according-to-transunion-cibils-latest-cmi-report/ ↩

-

CGAP, "Convenience Drives Rapid Adoption of Account Aggregators in India," April 2025. ~120M linked accounts by December 2024, up from 39M a year earlier; over $10B in loans enabled since the September 2021 launch. https://www.cgap.org/blog/convenience-drives-rapid-adoption-of-account-aggregators-in-india ↩

-

CGAP / Sahamati customer research, late 2024 (n=1,860). Of recent loan applicants, 21% recalled using AA data, up from 10% in 2023. https://www.cgap.org/blog/convenience-drives-rapid-adoption-of-account-aggregators-in-india ↩

-

PayU India, public commentary on its payment-network data and pre-underwriting capability. ↩

-

FinBox, KreditBee, EarlySalary, and CASHe product and engineering disclosures on alternative-data underwriting for thin-file and blue-collar applicants. ↩

-

Slice, reported portfolio metrics on starting limits and 90-day delinquency. ↩